There's something unique about mortgage rates for Americans that seems to elicit a visceral reaction. Maybe because it really feels like the rate comes from a bunch of ivory tower economists at the Fed, AND YET is so financially consequential and long-lasting for the average American.

"I've been hustling my ass off to save for a down-payment, why am I having to pay 6% now when my neighbor got 3% in 2021?"

I think that's one of the reasons Kaz's post on X has blown up so much - because mortgage rates really encapsulate the whole "unaffordability" conversation into a single number.

Anyways, it's clear to me that Opendoor's struck a rich vein here given by how much entrenched interests have come out of the woodwork complaining.

I try to lay out the economics and business case below:

Initially, I had thought Opendoor might be doing some partial buy-down / subsidy to get to the 4.99 rate but they've explicitly denied that.

This was further clarified when Kaz himself said that there are 65-85 bps of margin and inefficiencies in the system - this provides a helpful bridge from the current average ~6% rate to the 4.99% Opendoor rate.

Here are the rough cost-savings as I can make out:

- No loan officer / origination fees - because Opendoor is generating the mortgage leads directly from the buyer, it immediately saves 30bps in origination costs by not having to pay commissions.

- AI-native platform - using BETR as the best-in-class comp which currently saves ~40-50bps using their AI Tinman platform, my guess is Opendoor is seeing maybe 20-30bps of savings with something they built in ~6 weeks (could easily be more).

- Wholesaler relationships - My hunch is that they're working with Lennar to take advantage of their mortgage wholesaler relationships. This probably cuts out another 10-20 bps of overhead costs.

- Reduced underwriting risk - Because Opendoor owns the home, there's essentially no appraisal, loan officer adverse-selection, or seller fall-through risk which further improves the quality of the loans. My guess is this is worth another 5-10 bps of savings.

Running mortgages at break-even:

If you sum the 4 items above, this gets you to ~70bps in total savings leaving about 30bps of "BU margin" to get to the full 100bps net discount.

What I think most critics or doubters miss is that no other mortgage-only company (like BETR) can offer the full ~100bps discount because they need to actually make money on the mortgage itself.

However, for Opendoor, their situation is unique because they're optimizing for resale velocity and holding cost savings. In an ironic twist of fate, their inventory holding costs are so high (3-4bps per day) that running a breakeven mortgage product to reduce Days in Possession (DIP) actually makes a ton of sense.

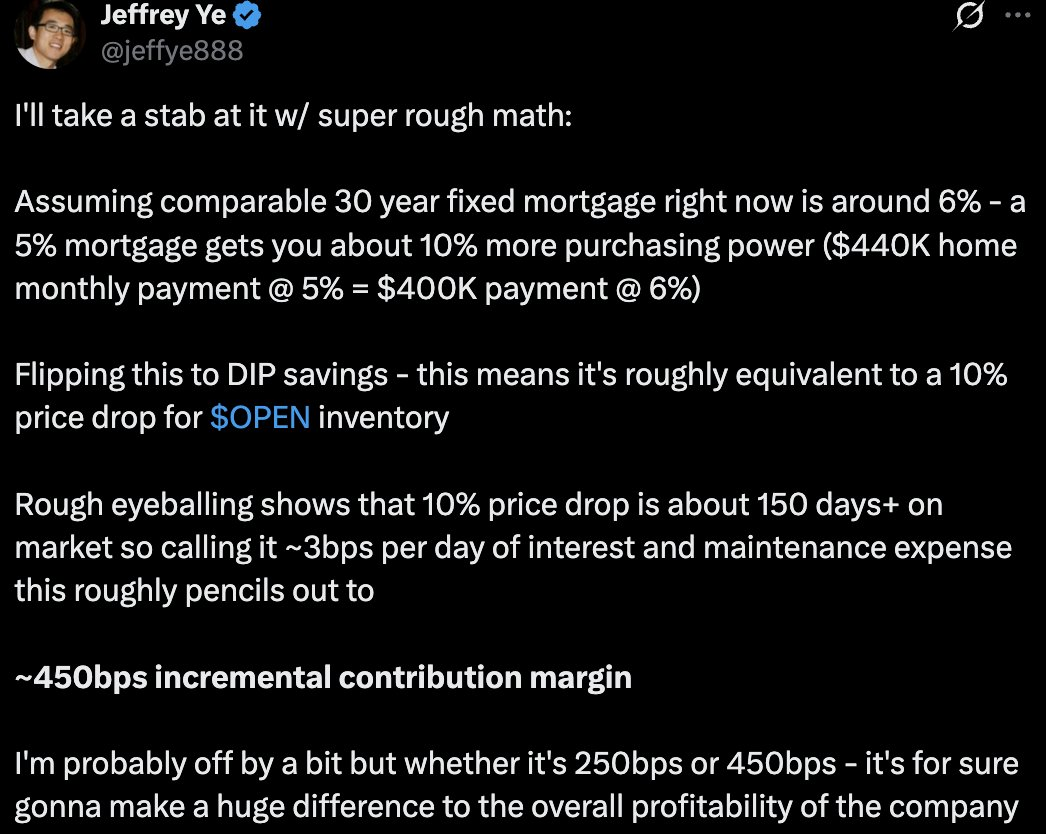

https://x.com/jeffye888/status/2027526312634814620

In other words, what Opendoor is in effect doing is taking the money they would've paid to their credit lenders and in property taxes / insurance and splitting those savings with buyers through the lower mortgage rate.

Because buyer purchasing power is so sensitive to rates and because Opendoor's holding costs are so high - they've actually just discovered a huge source of "alpha" for the business.

This is very analogous to what homebuilders have been doing for the last 3-4 years with buy-downs (but likely even more high-leverage given Opendoor's high holding costs). My guess is they're working closely with Lennar to learn and optimize the product for resale velocity.

All the above is a bit speculative but I think the general framework holds regardless of whether the numbers were off by a few bps here or there.

Lastly, I also have a sneaking suspicion that Opendoor's mortgage rate offering could be the "killer feature." Something SO compelling and SO economical that it could actually start to decalcify consumer behavior and make Opendoor.com a starting point for any homebuyer.

Only time will tell.